(615) 424-7773

Need help? Call me!

(615) 424-7773

Need help? Call me!

I will be happy to educate you on your many Medicare options and explain the differences between a Medicare Supplement and the Medicare Advantage Plans offered in TN.

Medicare Part A and Part B cover certain medical services and supplies in

hospitals, doctors’ offices, and other health care settings. Prescription drug

coverage is provided through Medicare Part D.

If you have both Part A and Part B, you can get all of the Medicare-covered

services listed in this section, whether you have Original Medicare or a

Medicare Advantage Plan or other Medicare health plan.

Part A (Hospital Insurance) helps cover:

Medicare Part B (Medical Insurance) helps cover medically necessary doctors’ services, outpatient care, home health services, durable medical equipment, mental health services, and other medical services. Part B also covers many preventive services.

Medicare doesn’t cover everything. If you need certain services that aren’t

covered under Medicare Part A or Part B, you’ll have to pay for them yourself unless:

Some of the items and services that Original Medicare doesn’t cover include:

A Medicare Advantage Plan is another way to get your Medicare coverage.

Medicare Advantage Plans, sometimes called “Part C” or “MA Plans,” are offered by Medicare-approved private companies that must follow rules set by Medicare. If you join a Medicare Advantage Plan, you’ll still have Medicare but you’ll get most of your Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance) coverage from the Medicare Advantage Plan, not Original Medicare. Most plans include Medicare prescription drug coverage (Part D). In most cases, you’ll need to use health care providers who participate in the plan’s network. However, many plans offer out-of network coverage, but sometimes at a higher cost.

Original Medicare pays for much, but not all, of the cost for covered health

care services and supplies. Medicare Supplement Insurance policies, sold

by private companies, can help pay some of the remaining health care

costs for covered services and supplies, like copayments, coinsurance,

and deductibles. Medicare Supplement Insurance policies are also called

Medigap policies. Some Medigap policies also offer coverage for services that Original Medicare doesn’t cover, like medical care when you travel outside the U.S. Generally, Medigap policies don’t cover long-term care (like care in a nursing home), vision or dental care, hearing aids, eyeglasses, or private-duty nursing.

Every Medigap policy must follow federal and state laws designed to protect

you, and they must be clearly identified as “Medicare Supplement Insurance.”

Insurance companies can sell you only a “standardized” policy identified

in most states by letters A through D, F, G, and K through N. All policies

offer the same basic benefits, but some offer additional benefits so you

can choose which one meets your needs.

Don’t worry, I can help, just fill out my contact form or call and I can answer any questions you might have to help you navigate through your medicare insurance options.

All information seen above can be read in full in the CMS MEDICARE AND YOU 2020 Handbook, along with a vast amount more information about your medicare insurance.

Medicare and You can be found here:

Most people don’t pay a Part A premium because they paid Medicare taxes while

working. If you don’t get premium-free Part A, you pay up to $565 each month.

If you don’t buy Part A when you’re first eligible for Medicare (usually when you turn

65), you might pay a penalty.

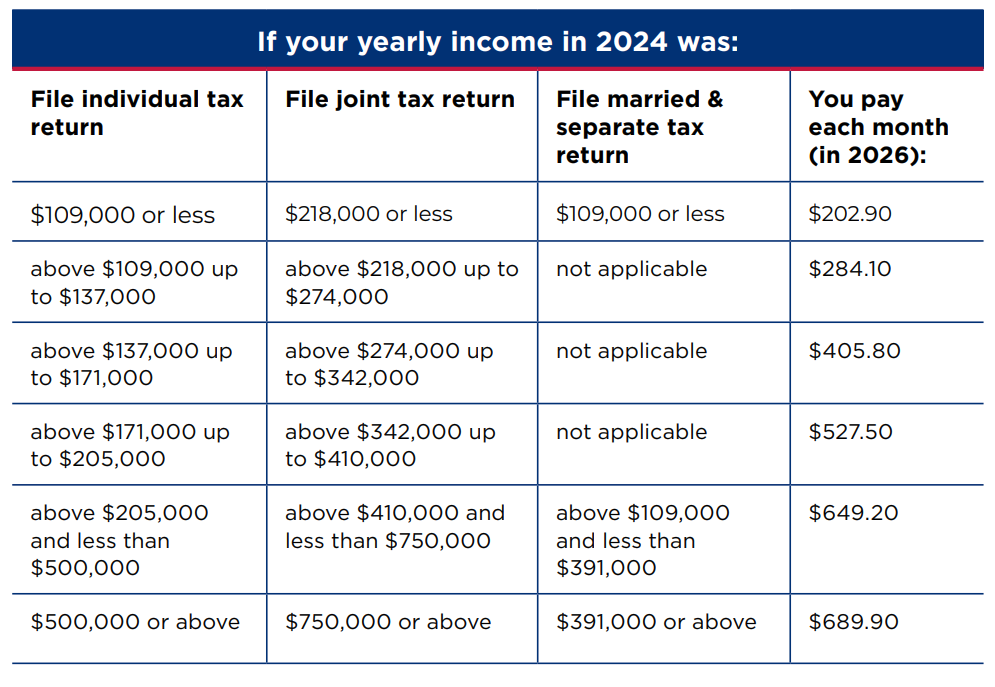

In 2026, you pay:

Most people pay the standard Part B monthly premium amount ($202.90 in 2026).

Social Security will tell you the exact amount you’ll pay for Part B in 2026.

You pay the standard premium amount if you:

If you have questions about your Part B premium, call Social Security at 1‑800‑772‑1213. TTY users can call 1-800-325-0778. If you pay a late enrollment penalty, these amounts may be higher.

You pay this deductible once each year.

Visit Medicare.gov/plan-compare to find and compare plan premiums. You can also

call 1‑800‑MEDICARE (1-800-633-4227). TTY users can call 1‑877‑486‑2048.

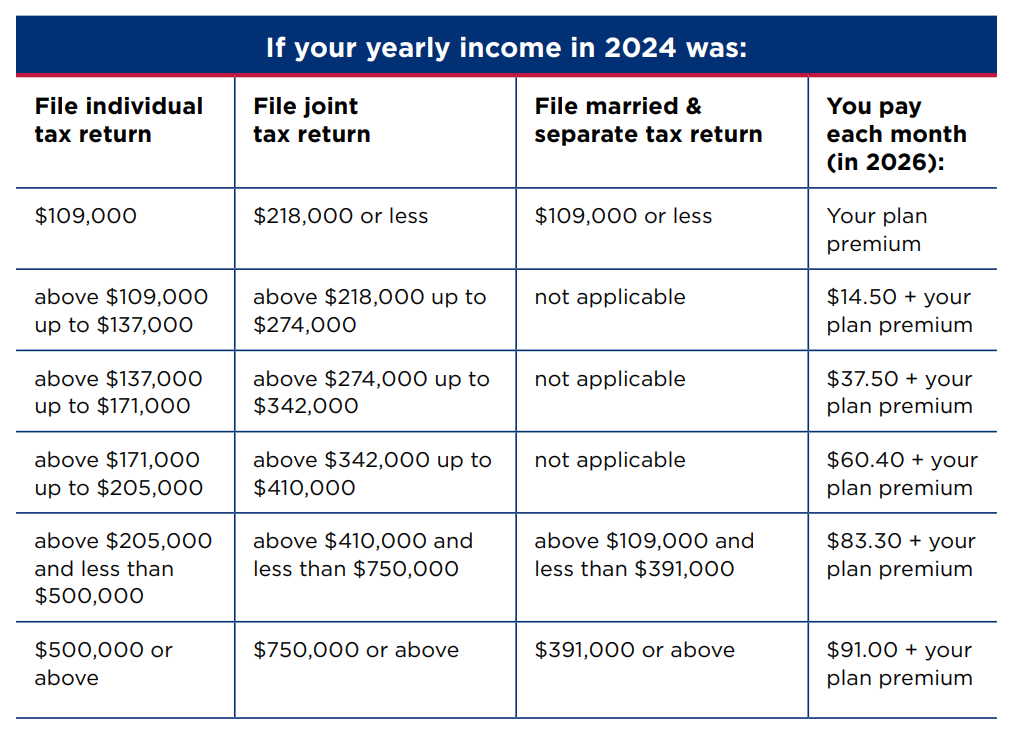

The chart below shows your estimated drug plan monthly premium based on

your income. If your income is above a certain limit, you’ll pay an income-related

monthly adjustment amount in addition to your plan premium.

Medicare uses the national base premium to estimate the Part D late enrollment

penalty and the income-related monthly adjustment amounts listed in the table

above. The national base amount can change each year. If you pay a late enrollment

penalty, your total premium amount may be higher.

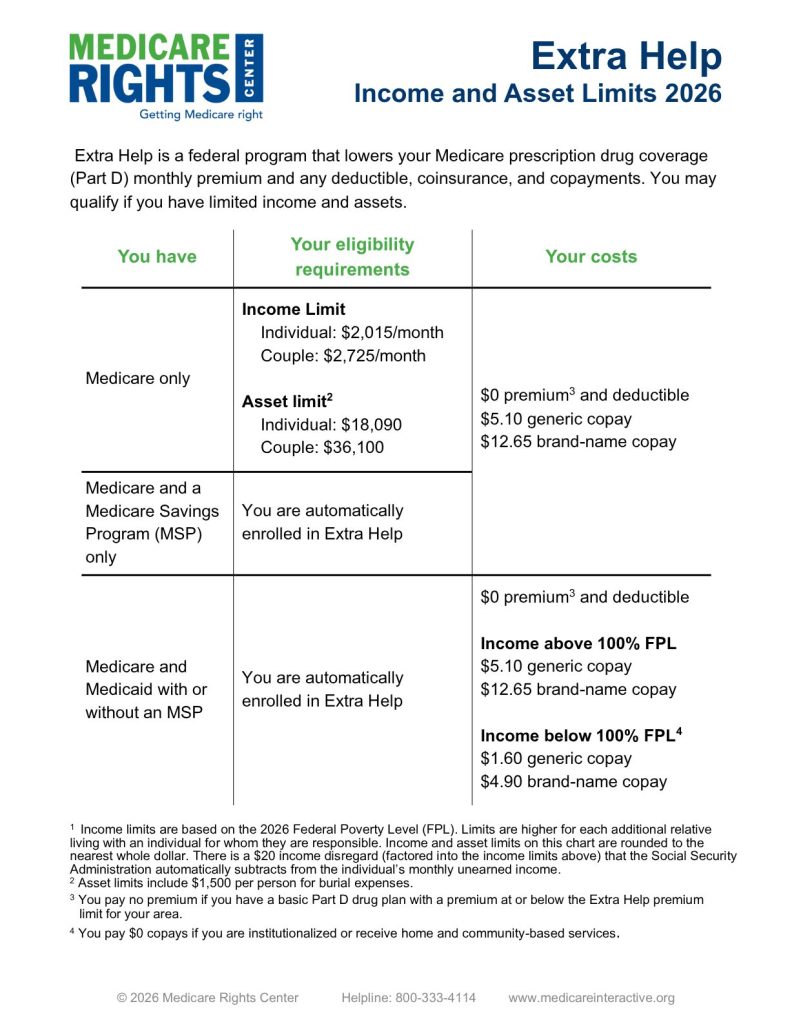

You may be able to get extra help to pay for the monthly premiums, annual deductibles, and co-payments related to the Medicare Prescription Drug program. However, you must be enrolled in a Medicare Prescription Drug plan to get this extra help.